What are Education Loans?

An education loan is financial assistance that helps students cover the costs of their university studies, whether in India or abroad. For studying abroad, different banks offer various types of loans depending on the country and field of study. You can use interest rates and loan terms to choose the loan that best suits your needs.

Let's say you've been accepted to a prestigious university abroad, ranked among the top 500 in the QS World University Rankings. This gives you access to better interest rates and opportunities to cover tuition fees and living expenses abroad.

However, applying for loans from different lenders can be overwhelming due to the numerous documents and procedures involved. Contact WayUpAbroad to guide you through this process. We help students find the best education loan that suits their study abroad needs, tailored to their specific circumstances, ensuring a smooth and hassle-free approval process.

How to Get Student Loan for Study Abroad?

When considering a student loan for studying abroad, students often overlook some details. Here are the steps you can follow to plan your student loan application:

- Identify the expenses you wish to cover during your studies.

- Calculate the estimated loan amount you need.

- Check the eligibility criteria of lenders.

- Prepare the required documents.

- Submit your loan application.

- Once approved, receive the loan and begin your study abroad journey.

You can Contact us for expert's help to complete your application. You can also connect us to search for available scholarships.

Expenses Covered in Loan for Study Abroad

The first step to getting a study abroad loan is calculating the expenses you need to cover. However, each lender has its own list of expenses. You can see the list below, but be sure to check with your lender. This will help you evaluate your options when applying for an education loan.

Tuition Fees:

All lenders cover these expenses, but the money is transferred directly to the university's account, not your personal account. This covers a significant portion of the loan amount.

Living Expenses:

Most lenders cover living expenses, but the specific expenses included vary. Living expenses include rent, electricity bills, and travel costs.

Health Insurance: Health insurance is mandatory for studying abroad, but only private banks cover the costs. So, plan accordingly and try to request health insurance coverage from your financial institution.

Visa Fees:

Not all lenders cover visa fees; some, such as non-bank financial institutions, offer them. Therefore, you will need to arrange your own visa fees.

Airfare:

No lender will cover the cost of airfare, but you should request that it be added to your list of expenses. Most lenders will agree to cover airfare.

Study Expenses:

Studying includes many expenses, such as books, laptops, study materials, graduation projects, study trips, and more. Most lenders cover these expenses, but if they are not, ask your lender to cover them.

Types of Education Loans for Abroad Studies

There are two types of education loans for studying abroad: secured loans and unsecured loans. You should understand the difference between them before choosing the one that's right for you.

Secured Education Loan:

When you get a secured loan from a lender, you provide collateral such as real estate, a fixed deposit, an insurance policy, etc., as security for the loan.

What is collateral?

Any movable or immovable property pledged as security for the loan is called collateral. Want to know about the types of collateral and the required documents? Read on.

What is the maximum secured loan amount?

The amount of a secured loan varies depending on the lender; however, it's usually between 70% and 80% of the value of the collateral.

Who is the guarantor?

What is the secured loan amount? When the loan amount exceeds ₹400,000, the bank requires a guarantor. The guarantor is a significant responsibility, as they are obligated to repay the education loan if the borrower defaults.

Advantages of a Secured Loan:

- Lower interest rate.

- Higher chances of approval.

- Longer repayment period.

- Possibility of obtaining a larger loan amount.

- No repayment required during the study period.

- No parental income required for approval.

Unsecured Student Loan:

When a borrower has no collateral to secure a loan, they typically opt for an unsecured student loan.

Advantages of an Unsecured Loan:

- Higher interest rate, usually 1.5% to 4% higher than a secured loan.

- Unsecured loans are riskier for the bank, making them more difficult to obtain and requiring a co-borrower.

- Relatively shorter repayment period.

- Part of the loan amount must be repaid during the study period.

- Parental income is required for approval.

Types of Lenders Offering Education Loans for Abroad Studies

When considering student loans for studying abroad, you have three main categories of lenders to choose from:

- Banks

- Non-bank finance companies

- International lenders

Lending options within each category are as follows:

Government Banks:

Traditional financial institutions offer education loans for studying abroad. Some of the most prominent lenders include:

State Bank of India (SBI):

The State Bank of India is a top choice for many government banks seeking an overseas study loan. It offers an overseas study loan under the Global Ed-Vantage program. Key features of the program include:

- Loan Amount: Up to ₹1.5 crore with collateral, and ₹50 lakh without collateral.

- Interest Rate: 9.65% for women and 10.15% for men.

- Loan Term: 15 years.

- Grace Period: The duration of the study period plus an additional 12 months.

- Exchange: Exchange options are available before and after repayment.

Punjab National Bank (PNB):

Some people turn to PNB for education loans. The bank offers loans for studying abroad under the "Udan" program. Key features of the education loan include:

- Loan amount: Up to 2 crore Indian rupees with collateral.

- Interest rate: 9.25% for male and female students at 50 listed universities. For non-listed universities, it is 10.50% for male students and 10.00% for female students.

- Loan term: 15 years.

- Grace period: The duration of the study period plus an additional 12 months.

- Disbursement: Disbursement options are available before and after repayment.

Private banks:

Many people turn to private banks when looking for unsecured education loans. Some of the most prominent banks include:

ICICI Bank:

ICICI Bank offers education loans to most universities. However, students who have been accepted to prestigious universities may be eligible for higher loan amounts. The key features of their education loan are:

- Loan amount: Up to INR 1.5 crore, with a minimum of INR 20 lakh.

- Interest rate: 10.25% for secured loans and 11.25% for unsecured loans.

- Loan term: 10 years.

- Grace period: The duration of your studies plus an additional 6 months.

- Conversion: Conversion options are available both before and after loan disbursement.

Note: ICICI Bank offers two categories: Premium and General. The Premium category includes the top 100 universities, while the General category covers almost all universities. Loan amount and interest rate may vary depending on the category.

Axis Bank:

- Axis Bank offers a wide range of universities with various benefits. The key features of their education loan for studying abroad are:

- Loan amount: Up to INR 1 crore with no collateral required.

- Interest rate: 11% to 11.5% depending on the category.

- Axis Bank Loan Term: 15 years Grace Period: Duration of studies plus an additional 6 months.

- Exchange: Exchange options are available before and after repayment.

Note: Axis Bank has two loan categories: Category A and Category B. These categories affect the interest rate and loan amount. You can borrow a minimum of INR 40 Lakh under Category A and INR 25 Lakh under Category B.

Non-Bank Finance Companies:

Non-bank finance companies are financial institutions that offer a variety of financial services similar to conventional banks, but operate without a banking license.

HDFC Credella:

Credella is an affiliate of HDFC Bank and offers competitive interest rates compared to other private banks. Key features of its Education Loan include:

- Loan Amount: Up to INR 75 Lakh with no collateral.

- Interest Rate: 11% per annum.

- Loan Term: 10 years Grace Period: Duration of studies plus an additional 6 months.

- Exchange: Exchange options are available before and after repayment.

Note: HDFC Credilla has three categories: A, B, and C. These categories are based on academic performance. The GRE is their preferred test for ranking students, but it is not mandatory.

Avans:

Avans offers student-specific education loans that cover various expenses within the loan amount. Key features of their education loan include:

- Loan amount: Up to ₹50 lakh with no collateral.

- Interest rate: 11.5%, depending on the category.

- Loan term: 15 years.

- Grace period: The duration of your studies plus 6 months.

- Disbursement: Disbursement options are available before and after repayment.

Note: Avans has three categories: A, B, and C. These categories affect the loan amount based on the university and academic performance. You can borrow a minimum of ₹30 lakh in category C.

International Lenders:

Financial institutions based outside your home country that specialize in providing international education loans for studying abroad.

M-Power:

M-Power may be a suitable option if you don't have a guarantor or collateral for your student loan. International lenders are often a last resort due to their higher cost for students. Key features of their student loans include:

- Loan Amount: Up to $100,000 USD with no collateral.

- Interest Rate: 9.99% per annum.

- Loan Term: 10 years.

- Grace Period: The duration of your studies plus an additional 6 months.

- Disbursement: Disbursement options are available both before and after repayment.

MPOWER Finance offers the Path2Success program, providing a comprehensive solution for students wishing to study in the USA or Canada. You can benefit from numerous advantages, including visa services such as free preparatory courses and mock interviews, financial services like pre-checking for opening US bank accounts and credit cards, and career guidance. Learn more about the Path2Success program.

Prodigy Finance:

Prodigy offers student loans for students wishing to study abroad. Its network includes more than 1,500 universities worldwide. Key features of its student loans include:

- Loan Amount: Up to 50 Lakh Indian Rupees with no collateral.

- Interest Rate: From 10.5% to 14%.

- Loan Term: 10 years.

- Grace Period: The duration of the study period plus an additional 6 months.

- Disbursement: Disbursement options are available before and after repayment.

Education Loan Interest Rates for Abroad Studies

Interest rates on student loans vary depending on the student's circumstances. The field of study, university, and country all play a significant role in determining the loan amount. However, the co-borrower's financial situation is another factor that influences the interest rate, particularly with unsecured loans. You can refer to the table below for interest rates from well-known lenders.

| Lender | Interest Rate (General / Male) | Interest Rate (Female) | Notes |

| SBI | 10.15% | 9.65% | 0.50% concession for women |

| UBI | Repo Rate + 2% | Repo Rate + 2% | Same rate for both |

| PNB | 10.50% | 10.00% | 0.50% concession for women |

| Axis Bank | 10.85% | 10.85% | No gender-based difference mentioned |

| ICICI Bank | 10.25% | 10.25% | — |

| IDFC First | 11.00% | 11.00% | — |

| Credila | 12.75% | 12.75% | — |

| Avanse | 12.75% | 12.75% | — |

| InCred | 11.85% | 11.85% | — |

| Auxilo | 11.50% | 11.50% | — |

| MPOWER | 9.99% | 9.99% | — |

| Prodigy | 10.50% | 10.50% | — |

Eligibility For Education Loan for Abroad

The requirements for obtaining a student loan to study abroad are straightforward, but may vary depending on the lending institution. The following are the general criteria for obtaining a student loan to study abroad:

- Nationality: Applicants must be Indian citizens.

- Admission: Guaranteed admission through merit or entrance examinations.

- Type of Study Program: Enrollment in professional study programs (Bachelor's/Master's).

- Academic Performance: A minimum score of 50% in the most recent qualifying examination.

- Guarantee: Guarantees may be required for secured loans.

- Joint Applicant: A joint applicant with good financial standing may be required for unsecured loans.

- University and Program Reputation: Considered when approving the loan.

Documents Required for Education Loan for Abroad Studies

Education loan required documents vary from lender to lender and also depend on the type of education loan applied for. Here’re the general documents required by almost every lender:

| Document Type | Required Document |

|---|---|

| KYC Documents |

|

| Address Proof |

|

| Academic Record Documents (From Applicant) |

|

| Financial Documents from the Co-applicant |

|

| Technical Documents for Collateral (For Secured Loan) |

|

| Legal Documents for Collateral (For Secured Loan) |

|

Key Features of Education Loan for Abroad Studies

When applying for an education loan, you should be aware of the key features that will help you choose the most suitable lender based on your financial situation.

- Loan Coverage: Ask the lender what expenses the education loan covers. Most lenders cover living expenses, tuition fees, and insurance costs.

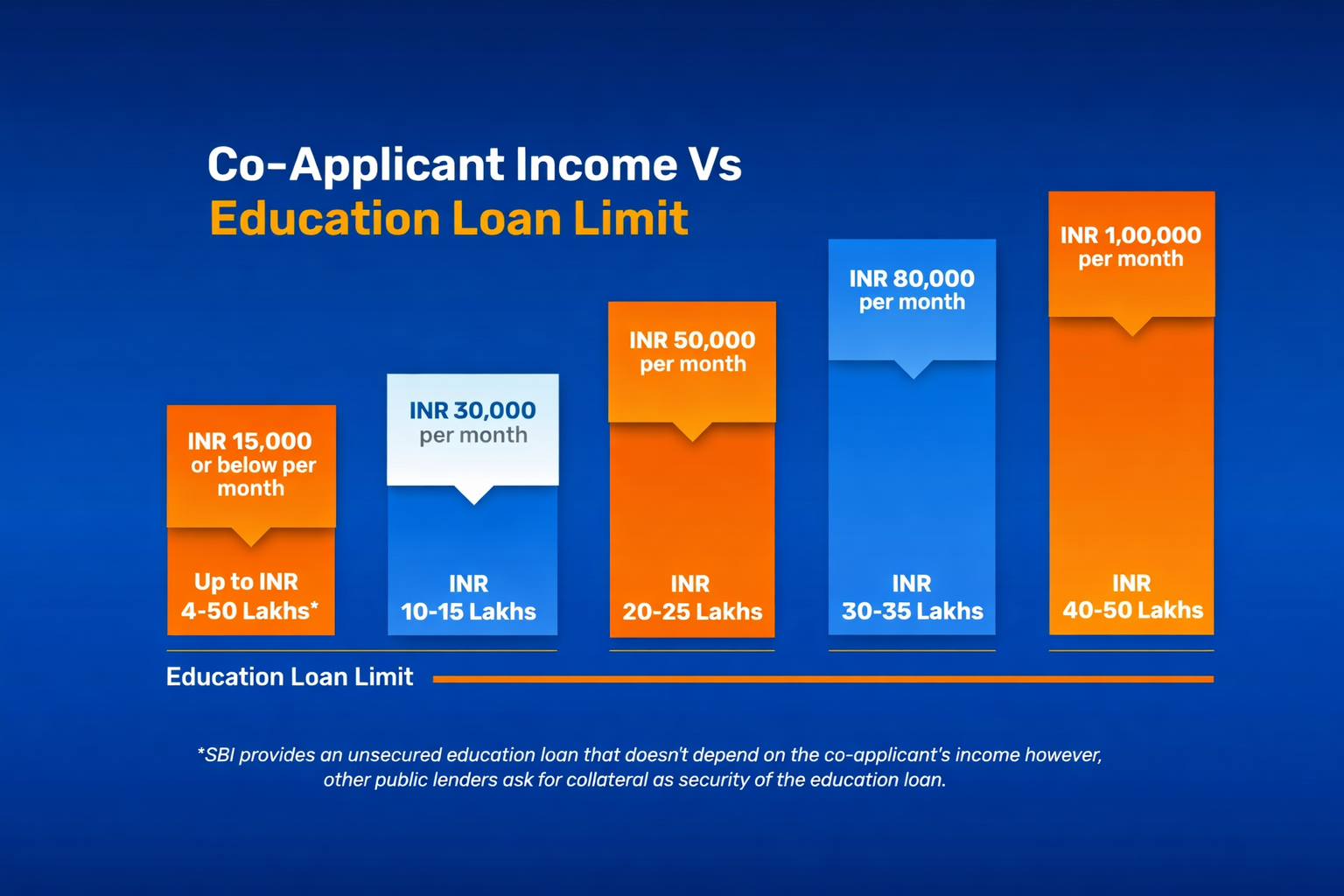

- Interest Rate: The lender sets the interest rate based on collateral or the co-borrower's creditworthiness. So, strengthen your financial profile by adding a co-borrower with good creditworthiness.

- Grace Period: Every lender offers a grace period, which includes the duration of your studies plus six months or a year. This period determines when your monthly repayments begin.

- Repayment Term: Most lenders offer repayment terms of up to 12 years. So, check with the lender about early repayment options and any associated penalties.

- Exchange Rate Protection: Many lenders offer exchange rate protection programs to safeguard your loan amount from currency fluctuations, ensuring stable repayment.

- Special loan programs: The government and universities offer programs that provide subsidies and reductions in processing fees and interest rates. Be sure to check your eligibility for these benefits.

Best Lenders to Get an Education Loan for Abroad Studies

The table below provides a comprehensive comparison of some of the best lenders offering student loans to help you choose the most suitable loan for studying abroad. The table includes detailed information on loan amounts, interest rates, grace periods, and other key factors to help you make an informed decision.

| Basis of Difference | UBI | SBI |

|---|---|---|

| Loan Amount (Unsecured) | Up to INR 40 Lakh | Up to INR 50 Lakh |

| Interest Rate | Starting at 9.8%* | 10.15% (Men)* 09.65% (Women)* |

| Moratorium Period | Course + 12 months | Course + 6 months |

| Unsecured Loan Eligibility | Only for master program | Top 100 universities |

| Financial Co-applicant Required* | Yes | Yes |

| Processing Fees | 10,000 INR + GST | 10,000 INR + GST |

| Processing Time | Up to 15-20 days | Up to 14 days |

| Margin Money | 10-15% | 10-15% |

| Repayment Tenure | 15 years | 15 years |

| Repayment Options* | Full Moratorium and PSI | Full Moratorium and PSI |

| Premiere Institute List | Have a list that can lead to fluctuation in interest rate | Have a list that includes the top 100 universities |

| Loan Approval Basis GRE / GMAT? | No | No |

| Tax Benefit* | Yes | Yes |

SI - Simple Interest; PSI - Partial Simple Interest; EMI - Equated Monthly Installment

*Interest rate as of January 2026

Private Banks:

| Basis of Difference | IDFC First Bank | ICICI Bank | Axis Bank |

|---|---|---|---|

| Maximum Loan Amount | Secured loans - INR 1 cr, Unsecured loans - INR 75 Lakh | Secured loans - INR 1 cr, Unsecured loans - INR 40 Lakh | Up to INR 40 - 75 Lakh |

| Interest Rate | 11.50 - 12.25% | 9.85 - 15.5% | 11 - 11.5% |

| Moratorium Period | Course period + 12 months | Course period + 6 months | Course period + 12 months |

| Unsecured Loan Eligibility | Only for master program | Only for approved courses | Only for approved courses |

| Financial Co-applicant Required* | Yes | Yes | Yes |

| Co-applicant Minimum Income | INR 35,000 / per month | INR 60,000 / per month | INR 35,000 / month |

| Processing Fees | 1 - 1.25% | 0.5 - 2% | 0.75% of the loan amount + GST |

| Processing Time | Up to 15-20 days | Up to 14 days | - |

| Margin Money | Nil | 0 - 15% | 0 - 5% |

| Repayment Tenure | 12 years | 8 - 12 years | 15 years |

| Repayment Options* | Simple or Partial Interest | Simple Interest (SI) | Simple Interest (SI) |

| Pre-approved College Lists | Colleges and universities are divided into three categories i.e. Platinum, Titanium, and Gold | Colleges and universities are divided into four categories i.e A1, A2, A3 & A4 | Colleges and universities are divided into four categories A, B, C, and D |

| Loan Approval Basis GRE / GMAT? | Yes | No | Yes |

| Tax Benefit* | Yes | Yes | Yes |

*Interest rate as of January 2026

NBFCs:

| Features | HDFC Credila | Avanse | Auxilo | InCred |

|---|---|---|---|---|

| Maximum loan amount | INR 20 - 75 Lakh | INR 20 - 75 Lakh | INR 20 - 75 Lakh | INR 20 - 80 Lakh |

| Interest rate* | 11.25 - 13% | 12.25 - 14% | 12 - 13.25% | 11.65 - 13.5% |

| Moratorium period | Course period + 1 year | Course period + 1 year | Course period + 1 year | Course period + 1 year |

| Unsecured loan eligibility | Only for master program | Only for master program | Only for master program | Only for master program |

| Financial co-applicant required* | Yes | Yes | Yes | Yes |

| Minimum co-applicant income (negotiable for secured education loans) | INR 30,000 - 60,000 | INR 30,000 - 60,000 | INR 20,000 - 40,000 | INR 20,000 - 40,000 |

| Processing fee | 0.5 - 1.5% of the loan amount + GST | 1 - 2% of the loan amount + GST | 0.5 - 1.5% of the loan amount + GST | 0.5 - 1% of the loan amount + GST |

| Processing time | Up to 7-10 days | Up to 14 days | Up to 5-7 days | Up to 10 days |

| Margin Money | Nil | Nil | Nil | Nil |

| Repayment tenure | 12 - 15 years | 12 - 15 years | 12 - 15 years | 12 - 15 years |

| Repayment Options During Moratorium* | Simple Interest (SI) or partial Simple Interest (PSI) | Simple Interest (SI) or partial Simple Interest (PSI) | Simple Interest (SI) or partial Simple Interest (PSI) | Simple Interest (SI) or partial Simple Interest (PSI) |

| Tax benefit* | Yes | No | No | No |

*Interest rate as of January 2026

Advantages of Abroad Education Loan

If you take out an education loan to study abroad, you can benefit from the following advantages:

- You can finance your studies abroad.

- You can customize your education loan repayment plans.

- You can take advantage of government support programs.

- Many lenders offer a grace period, making your studies easier.

- You can benefit from Section 80E tax relief on the interest rate.

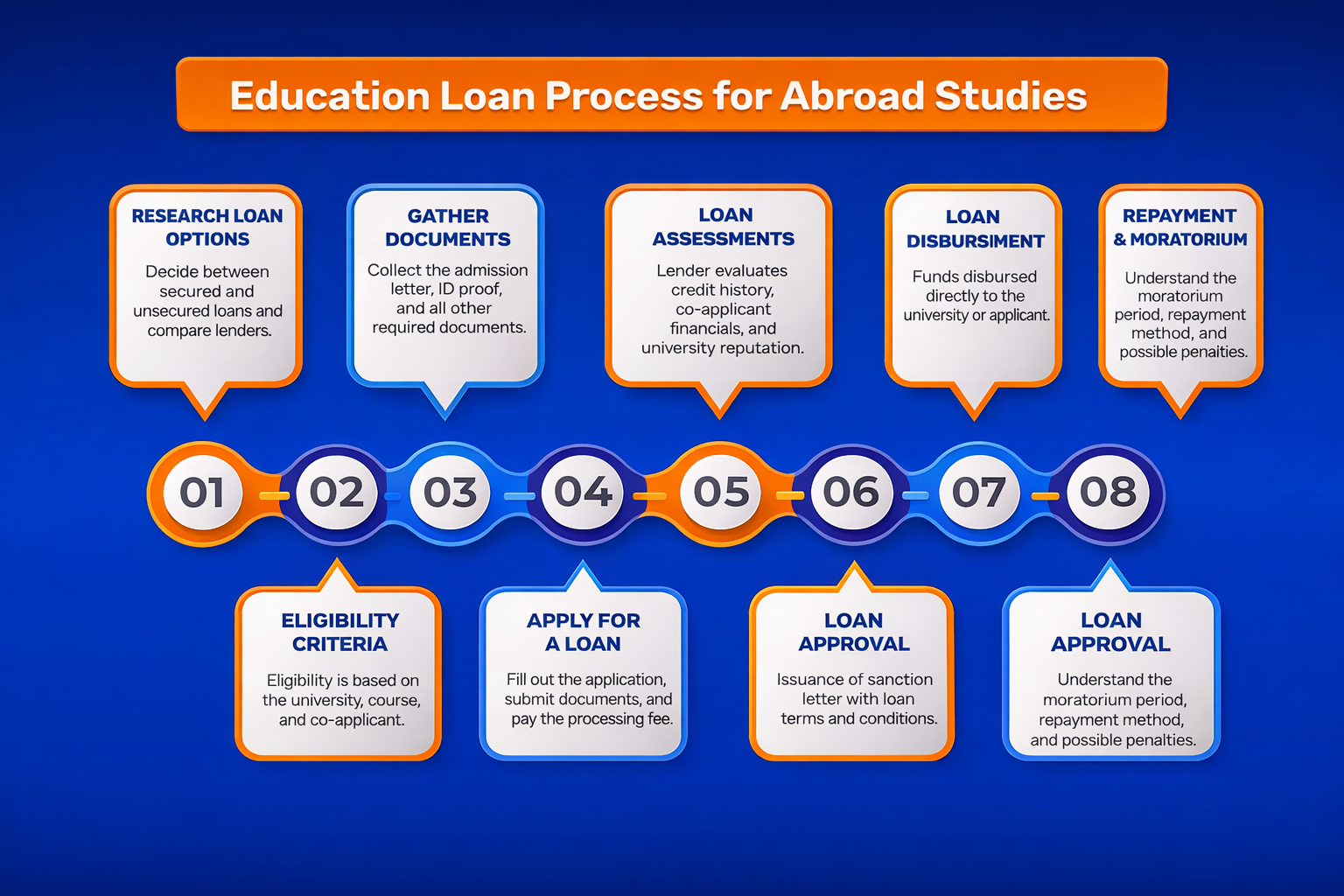

How Do I Apply for an Student Loan for Abroad?

Applying for student loans to study abroad can be straightforward if done carefully. To help you answer the question, "How do I get a student loan to study abroad?", here are some steps to guide you.

- Checking Eligibility with WayUpAbroad: WayUpAbroad assesses your profile and selects the best lender for you, making the loan application process easier.

- Connecting with a Student Loan Advisor: A WayUpAbroad student loan advisor will contact you to help you understand everything about studying abroad loans and your chosen lender. The advisor will also provide you with a list of required documents.

- Submitting and Verifying Documents: WayUpAbroad simplifies the document submission process by offering a home collection service or a dedicated online download list. Once you submit your application, WayUpAbroad handles all the remaining procedures and works with the lender to efficiently verify your documents.

- Loan Approval and Disbursement: After all your documents have been verified, you will receive a loan approval letter and an agreement to sign. Once all of this is completed, you can receive the loan amount as it suits you.